Gurgaon is no longer just a real estate market driven by appreciation—it has evolved into a structured ecosystem of micro-markets where rental yield, tenant demand, and long-term wealth creation vary significantly from one corridor to another.

In 2026, building passive income through real estate is no longer about simply purchasing a property and putting it on rent. It requires a strategic approach that combines location intelligence, asset selection, financial discipline, and long-term scaling.

For investors exploring high rental yield properties Gurgaon, the real question is not “what to buy,” but “where and why to buy.”

This guide explains how serious investors are structuring portfolios to generate ₹1 lakh or more in monthly passive income from Gurgaon real estate.

Why Gurgaon Works for Passive Income in 2026

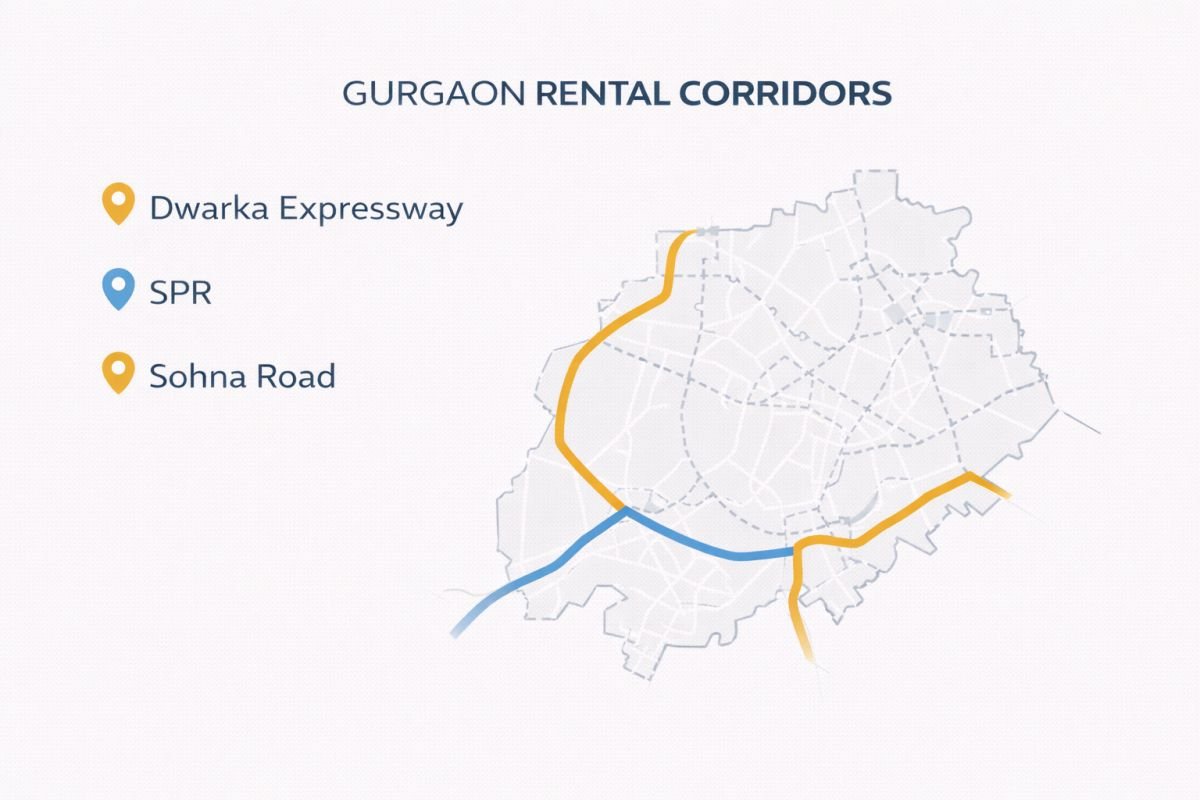

What makes Gurgaon unique is its corridor-driven rental ecosystem. Unlike many cities where rental performance is relatively uniform, Gurgaon behaves as a network of independent micro-markets, each with its own demand drivers, tenant profile, and yield potential.

For instance, Dwarka Expressway is currently driven by infrastructure growth and improving connectivity, which is gradually strengthening rental absorption. In contrast, Golf Course Extension Road attracts a premium tenant base, largely consisting of corporate professionals and expatriates. New Gurgaon sectors, particularly 82 to 95, offer consistent mid-segment rental stability, while Sohna Road balances affordability with strong tenant demand.

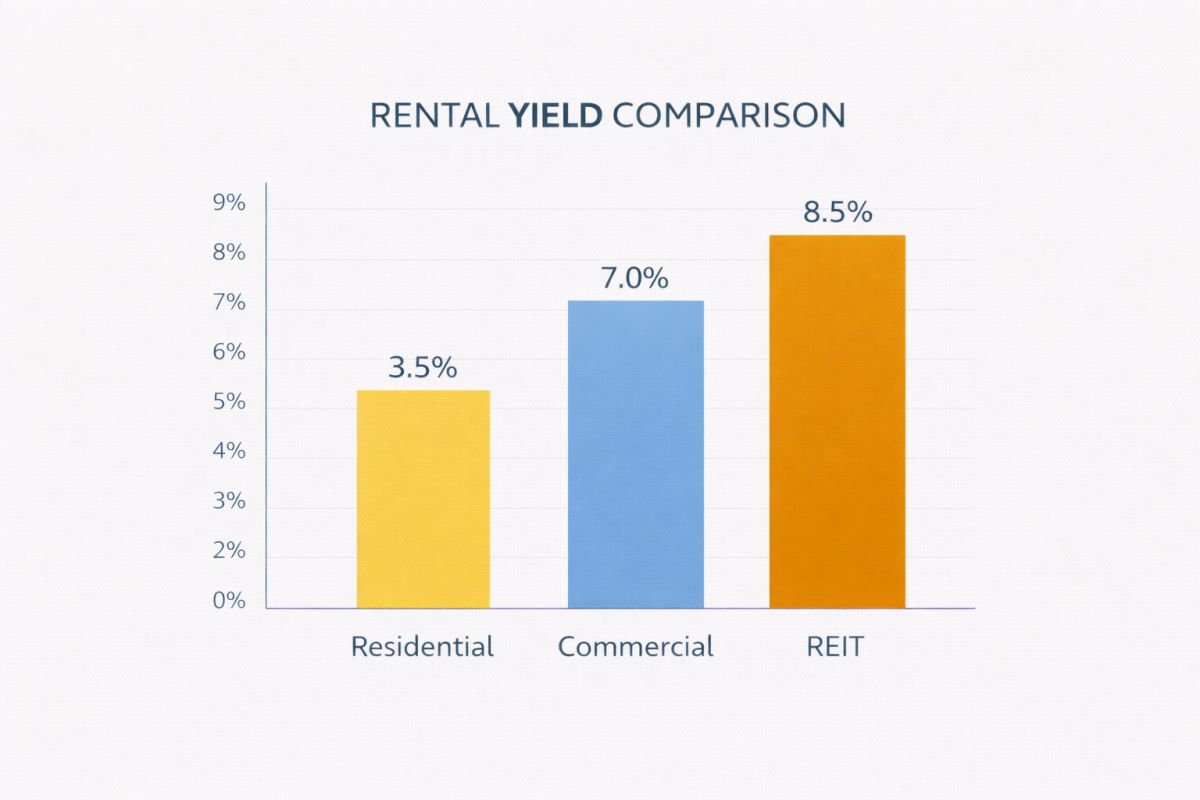

As of 2026, rental yields vary significantly across asset types. Residential properties typically deliver between 2.8% and 4.5%, while builder floors in mid-segment sectors can reach around 3.5% to 4%. Premium high-rise apartments tend to operate at lower yields of 2.5% to 3.2%, whereas pre-leased commercial assets offer much higher returns in the range of 6% to 8%. REIT investments, on the other hand, provide relatively stable dividend yields of 5% to 7%.

To accurately identify the best locations for rental income Gurgaon, investors must evaluate not just pricing trends but also employment hubs, infrastructure access, and tenant behavior.

Gurgaon offers a powerful combination of cash flow, appreciation, and leverage-driven wealth creation—but only when the investment strategy aligns with corridor dynamics.

What Does ₹1 Lakh Monthly Passive Income Actually Require?

A realistic understanding of numbers is critical before entering rental investing.

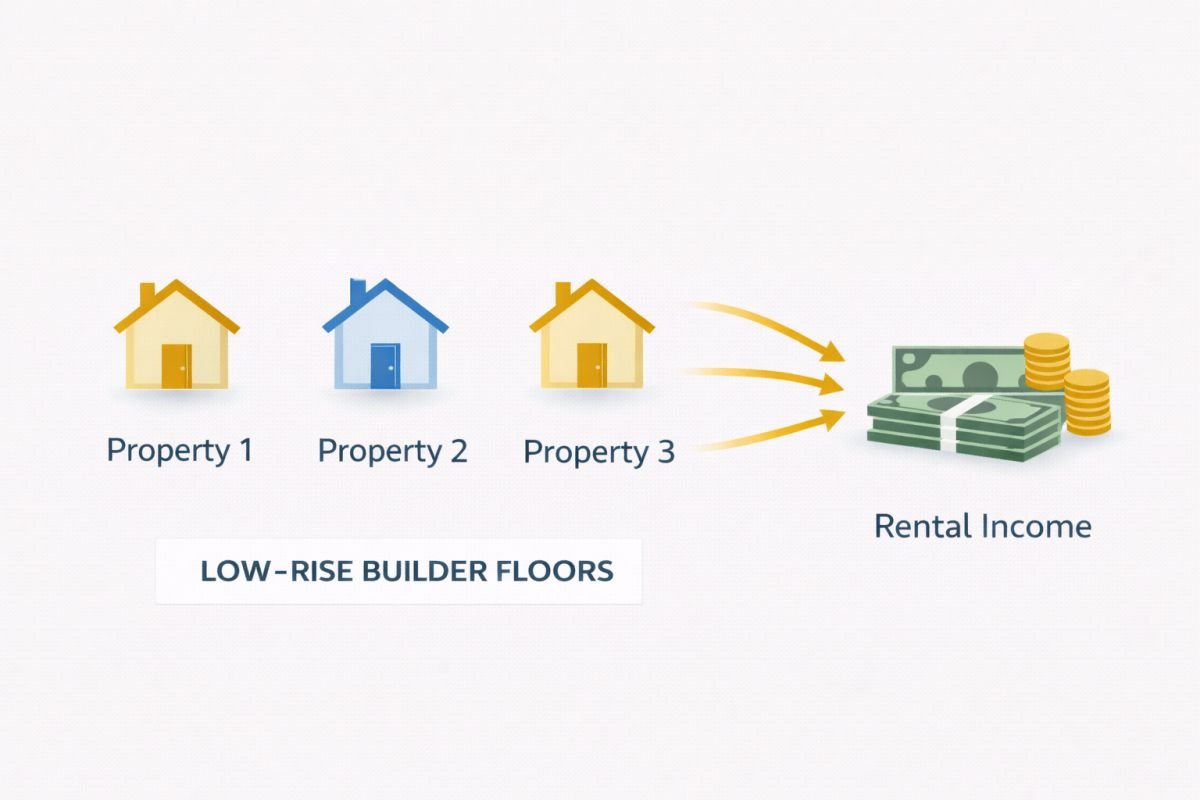

In the current Gurgaon market, a typical residential rental property generates a net monthly surplus of approximately ₹20,000 to ₹30,000 after accounting for EMI, maintenance, and vacancy buffers. Based on this, reaching a monthly passive income of ₹1 lakh requires a structured portfolio rather than a single asset.

Most investors achieve this through either three to five well-selected residential properties, a hybrid mix of two commercial assets and one residential unit, or a diversified combination of residential real estate, REIT exposure, and pre-leased commercial investments. The exact structure depends on capital availability, risk tolerance, and long-term financial goals.

Builder Floors vs High-Rise Apartments: Income vs Growth

One of the most important decisions investors face is choosing between builder floors and high-rise apartments. This decision directly impacts both rental income and long-term appreciation.

Builder floors, especially in mid-segment sectors, generally offer better rental efficiency due to lower entry cost and reduced maintenance overhead. They are particularly effective for investors seeking immediate cash flow. However, their appreciation trajectory tends to be moderate compared to large-scale developments.

High-rise apartments, on the other hand, attract stronger tenant preference and offer better resale liquidity. They are also better positioned to benefit from infrastructure-led growth, especially in corridors like Dwarka Expressway. While their rental yield may be slightly lower, they compensate through long-term capital appreciation.

In simple terms, builder floors are more aligned with income generation, while high-rises balance income with growth potential.

Rental Yield Snapshot Across Gurgaon Corridors (2026)

Rental performance varies significantly depending on both corridor and asset type. The table below provides a realistic comparison.

| Corridor | Residential Yield | Commercial Yield | Appreciation Bias |

|---|---|---|---|

| Dwarka Expressway | 2.8% – 3.5% | 6% – 7% | High |

| Golf Course Extension Road | 2.5% – 3.2% | 6% – 8% | Stable Premium |

| New Gurgaon (82–95) | 3.5% – 4% | ~6% | Moderate |

| Sohna Road | 3% – 3.8% | 6% – 7% | Balanced |

This comparison clearly shows that mid-segment corridors often deliver better yield efficiency, while premium corridors provide stability and long-term value.

Co-Living: A High-Yield Alternative Strategy

Another emerging segment in Gurgaon is co-living investment opportunities Gurgaon, which focuses on renting individual rooms instead of entire units.

This model can significantly increase rental yield due to better space utilization and strong demand from young professionals. However, it also requires active management, furnishing investment, and operational involvement. For investors willing to take a hands-on approach, co-living can outperform traditional rental models.

Commercial Assets & REITs: Strengthening Cash Flow

Pre-leased commercial properties offer one of the most stable and high-yield investment options in Gurgaon. These assets typically generate 6% to 8% annual returns and come with structured lease agreements, including lock-in periods and periodic rental escalation clauses.

However, they also carry risks such as tenant dependency and sensitivity to economic cycles.

For investors seeking liquidity and lower operational involvement, REITs provide an alternative. They offer exposure to Grade A commercial real estate without the need to manage tenants directly. While they lack leverage benefits, they ensure regular income and flexibility.

A well-balanced portfolio often includes a mix of residential assets, commercial investments, and REIT allocation to optimize both yield and risk.

Advanced Metrics: How Serious Investors Evaluate Returns

While most investors focus only on rental yield, experienced investors rely on deeper financial metrics.

Gross rental yield provides a basic understanding of returns, but net yield—after accounting for maintenance, taxes, and vacancy—is far more accurate. Beyond this, cash-on-cash return becomes the most critical metric, as it measures the actual return on invested capital, especially when leverage is involved.

This is where professional investing differs from casual property buying.

Financing Strategy & Risk Management

In 2026, home loan interest rates in the NCR region typically range between 8% and 9.5%. This makes financial discipline extremely important.

Successful investors ensure that their EMI does not exceed 70–75% of expected rental income. They also maintain a reserve buffer equivalent to at least six months of EMI and test their investment against potential rental declines.

Leverage is a powerful tool—but only when used responsibly.

A Smarter Approach for Salaried Investors

For working professionals, building a rental portfolio requires careful planning and gradual scaling. Following a structured approach like real estate investment strategy for salaried professionals helps in balancing income stability with long-term wealth creation.

This approach focuses on affordability, risk management, and phased expansion rather than aggressive investment.

Realistic Scaling Example (₹1.5 Cr Capital)

A practical example highlights how passive income is built over time.

An investor may begin with a ₹70 lakh high-rise generating ₹28,000 monthly rent, followed by a ₹50 lakh builder floor generating ₹22,000. The remaining capital can be allocated to REIT investments for additional income and liquidity.

This combination can generate approximately ₹85,000 to ₹1,05,000 per month. Over time, as property values appreciate, refinancing can unlock additional capital to acquire more assets, enabling further income growth.

Final Thought: Passive Income Is Built, Not Bought

Passive income in Gurgaon real estate is not created through random purchases or short-term trends. It is the result of a disciplined, long-term strategy based on location intelligence, realistic yield expectations, and diversified asset allocation.

The investors who succeed in this market are not those chasing hype, but those aligning their investments with rental demand, financial structure, and future growth potential.

If you are planning your next move, explore best investment opportunities Gurgaon 2026 that are backed by real rental demand and not just appreciation narratives.

Frequently Asked Questions About Building Passive Income in Gurgaon Real Estate (2026)

How much capital do I realistically need to start building meaningful passive income in Gurgaon real estate?

Most investors underestimate this. In Gurgaon’s current 2026 environment, building serious monthly passive income typically requires deployable capital of at least ₹50–75 lakh if leverage is involved. If the goal is ₹1 lakh per month net income, you’re usually looking at ₹1.2–2 crore in structured allocation across residential and possibly commercial assets. The exact number depends on whether you prioritize yield-heavy builder floors, appreciation-led high-rises, or a hybrid model including REIT exposure. Passive income here is not about one property — it’s about capital structure.

Is rental income in Gurgaon stable enough to depend on long-term?

In well-selected corridors like Dwarka Expressway, Golf Course Extension Road, and established parts of New Gurgaon, rental demand has remained structurally supported by corporate migration, infrastructure expansion, and professional tenant bases. However, stability depends heavily on micro-market selection. Oversupplied sectors can experience temporary rental stagnation. Investors who choose strong connectivity corridors and maintain a vacancy buffer generally experience consistent income, but treating rental income as “guaranteed” without stress testing is risky.

What actually gives better long-term returns in Gurgaon — rental yield or appreciation?

In Gurgaon, appreciation often plays a bigger role than pure rental yield. Residential yields typically range between 2.8% and 4%, which alone may not look aggressive. However, infrastructure-led corridors such as Dwarka Expressway historically demonstrate stronger appreciation cycles once occupancy and connectivity stabilize. Investors who combine rental cash flow with 5–7 year appreciation cycles and refinance intelligently often outperform those chasing yield alone. The real power is in the combination of yield, leverage, and appreciation timing.

Is buying a pre-leased commercial unit safer than residential rental for passive income?

Pre-leased commercial assets can offer higher yields, often in the 6–8% range, but safety depends on tenant quality and lock-in structure. A long lock-in with a strong corporate tenant provides predictable income, but vacancy risk is more concentrated — losing one tenant can halt cash flow entirely. Residential rental, on the other hand, usually has lower yield but broader tenant depth. Commercial can generate stronger monthly income, but it requires stricter due diligence and risk tolerance.

If interest rates rise, does passive income from Gurgaon property become risky?

Interest rate sensitivity is one of the biggest overlooked factors. With floating home loan rates typically ranging between 8% and 9.5% in NCR during 2026, even a 1% rate increase can significantly reduce monthly surplus if EMIs are stretched. Investors who keep EMI below 70–75% of expected rent and maintain at least six months of reserve cushion generally remain stable even in tightening cycles. Passive income becomes risky only when leverage is aggressive and reserves are thin.

Join The Discussion