Buying property in Gurgaon is not just about choosing the right sector or builder—it is a long-term financial decision that will shape your cash flow for the next 20–25 years.

In high-value markets like Dwarka Expressway, Golf Course Extension Road, and New Gurgaon, even a small mistake in loan structuring can cost more than a slightly overpriced property. Most buyers focus only on interest rates, but serious buyers evaluate eligibility, EMI sustainability, lender flexibility, and risk exposure.

Before structuring your loan, it’s important to understand the complete buying journey—from selection to registry. Start with this complete property buying guide Gurgaon.

Because without clarity on the full process, even the best financing plan can fail.

Why Home Loan Planning Matters More Than Price Negotiation

At Gurgaon’s typical ticket size—₹90 lakh to ₹3 crore—loan structure becomes more important than marginal price differences.

A 0.25% interest variation can translate into lakhs over the loan tenure. More importantly, EMI miscalculation can create long-term financial pressure, especially when combined with rent, lifestyle expenses, and other liabilities.

This is why intelligent buyers focus on affordability and sustainability, not just eligibility.

Home Loan Eligibility: How Much You Can Actually Borrow

Most buyers ask how much loan they can get, but the better question is how much loan they should take.

Eligibility depends on income, existing liabilities, credit score, and debt-to-income ratio. In Gurgaon, property value also plays a major role, as higher ticket sizes reduce funding percentages.

For example, on a ₹1.5 crore property, banks may fund only 70–75%, which means you need a significant upfront contribution—including statutory costs like stamp duty.

This is where buyers often face liquidity pressure because they calculate EMI—but not total cash requirement.

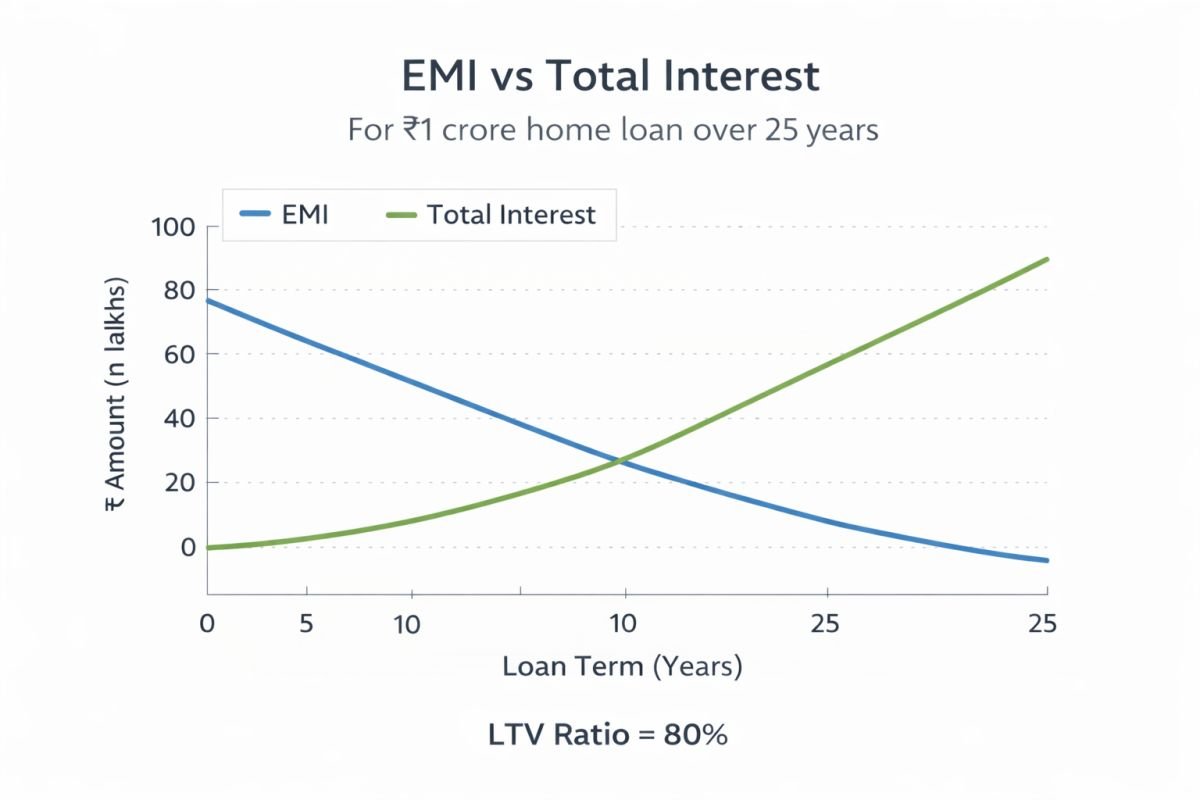

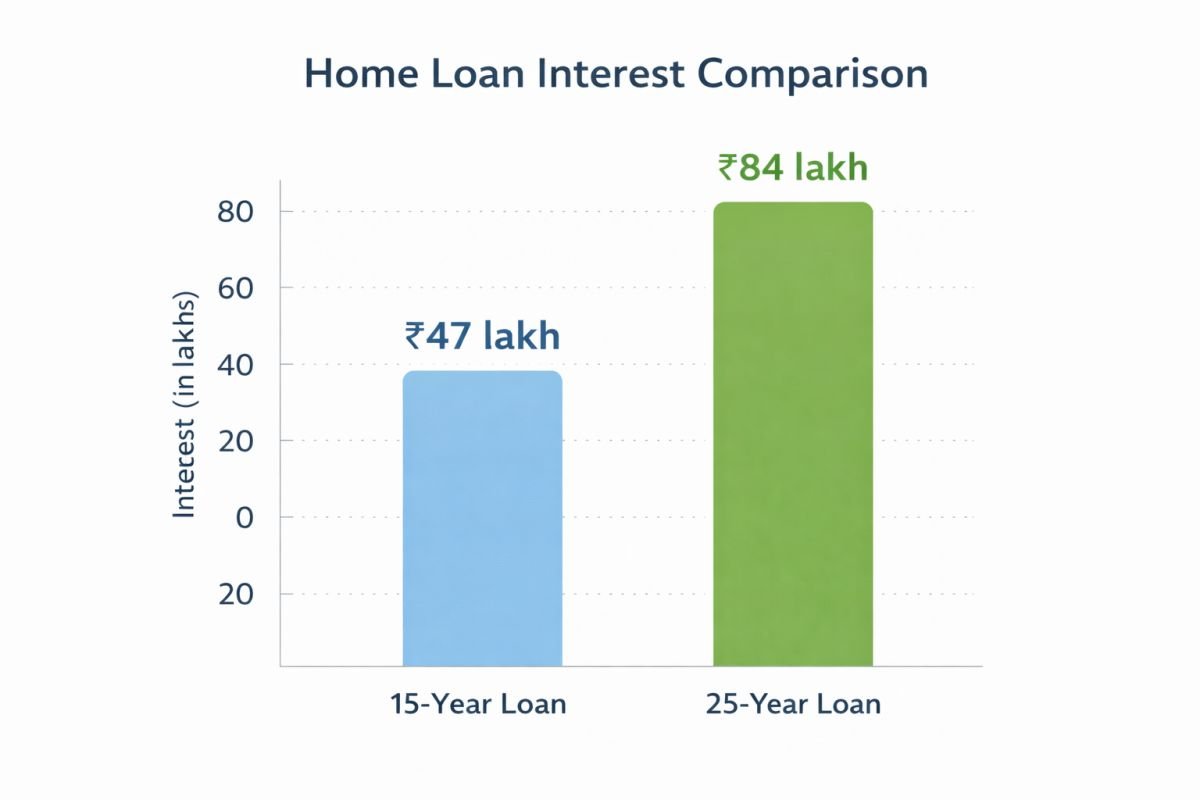

EMI Reality: What a ₹1 Crore Loan Actually Means

A ₹1 crore home loan at current interest rates typically results in an EMI between ₹80,000–₹90,000 depending on tenure.

However, the real impact is not the EMI—it’s the total interest paid over time, which can exceed ₹1.3 crore over a 25-year period.

Extending tenure reduces EMI but increases total cost significantly. Reducing tenure increases EMI but improves long-term savings.

The right balance depends on your income stability and risk tolerance—not just affordability.

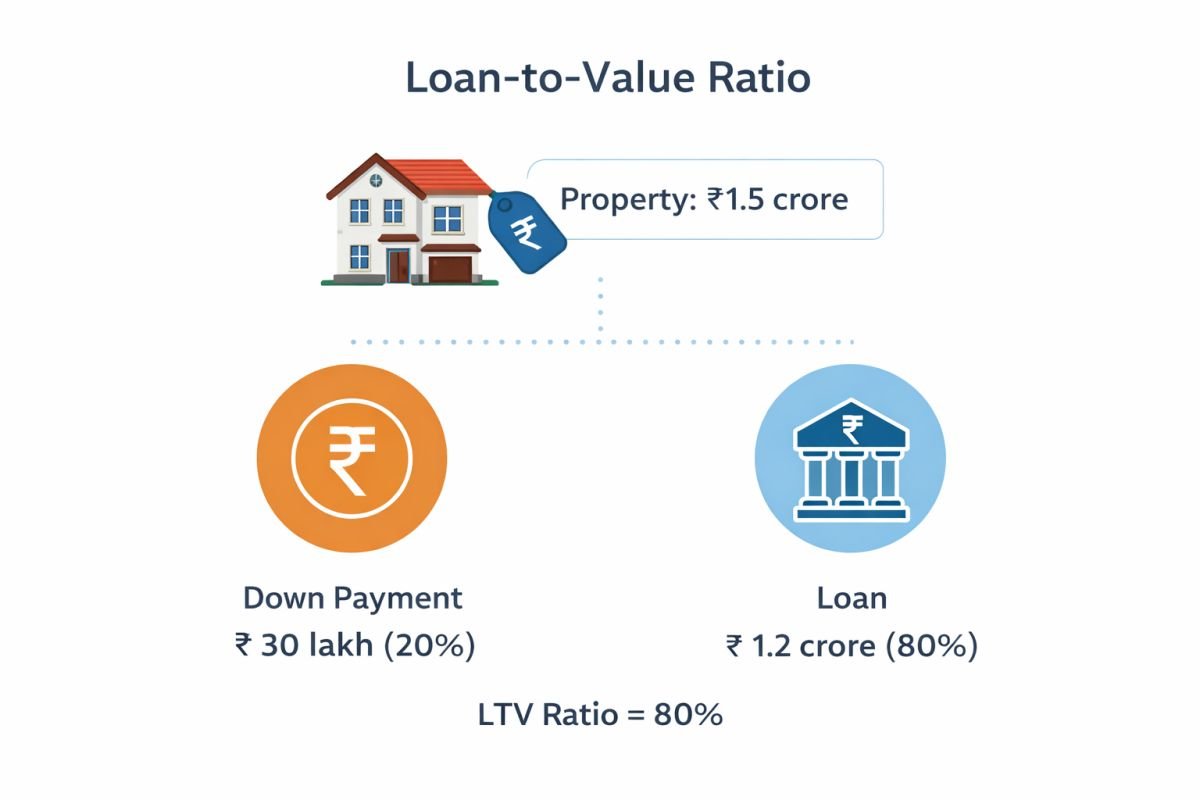

Loan-to-Value (LTV): The Hidden Constraint

For high-value properties in Gurgaon, LTV ratios are stricter.

Banks usually fund:

- 75–80% for mid-range properties

- 70–75% for higher ticket sizes

This increases your down payment requirement and directly impacts liquidity.

Many buyers lose deals not because they lack eligibility—but because they underestimate upfront capital.

Hidden Costs: Why Loan Planning Alone Is Not Enough

Even if your loan is approved, your total cost includes more than just EMI.

Stamp duty, registration, GST, maintenance deposits, and other charges significantly increase your financial commitment. Ignoring these leads to last-minute funding gaps.

To understand the full cost structure, review hidden costs in property purchase.

Because financing a property without understanding total cost is incomplete planning.

Stamp Duty & Legal Costs: The Non-Financed Component

Banks do not fully finance stamp duty and registration charges. These must be paid from your own funds.

On high-value transactions, this can add ₹10–20 lakh to your upfront requirement.

Before finalizing any loan, make sure you clearly understand stamp duty and registration charges explained.

Because your loan may get approved—but your liquidity might still fall short.

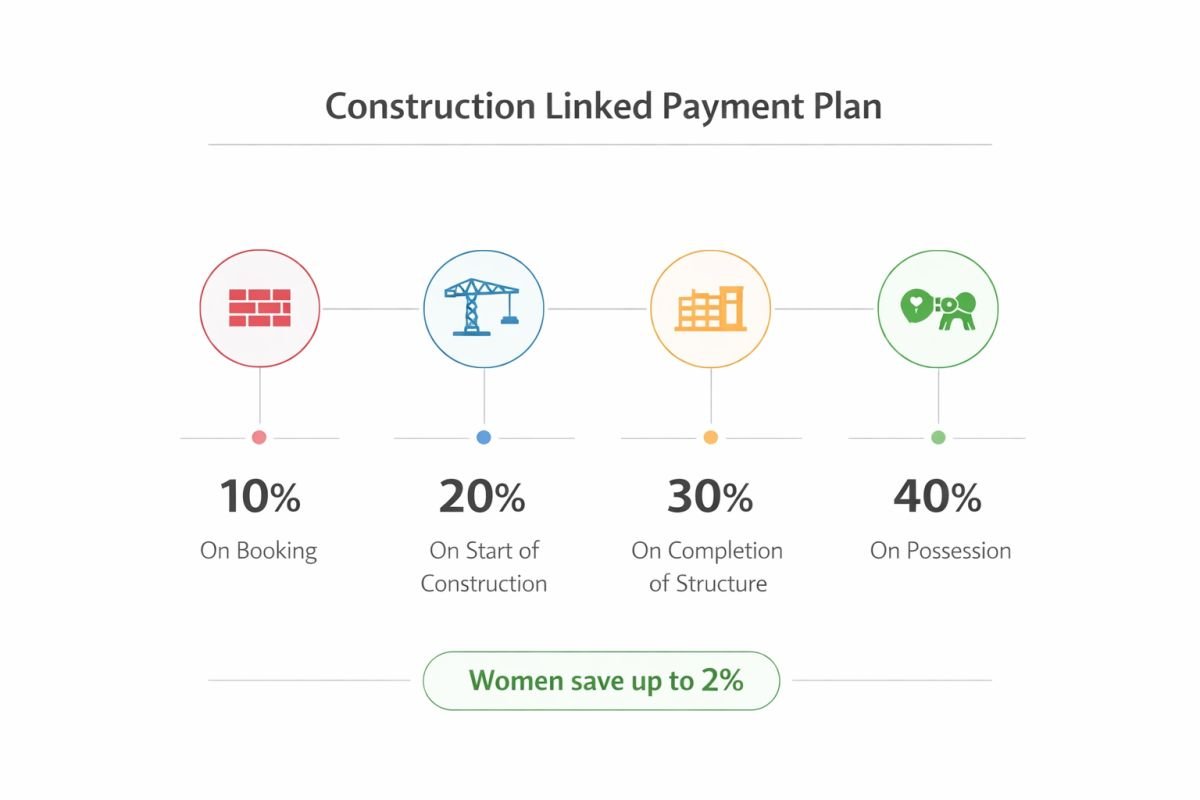

Payment Plans: Where Financial Risk Changes

Payment structure plays a major role in how your loan behaves.

Construction-linked plans reduce risk because payments are tied to progress. Backend-loaded plans increase pressure later. Subvention schemes shift risk depending on developer execution.

Choosing the wrong structure can create stress even if your loan is well planned.

If you’re evaluating structured payment options, explore projects offering easy payment plans.

Because the way you pay is as important as how much you pay.

Legal & Documentation: What Lenders Actually Check

Loan approval is not just about income—it’s also about property risk.

Banks evaluate:

- Title clarity

- RERA registration

- Builder credibility

- Approval status

- Construction stage

If the project fails these checks, your loan may be delayed or rejected.

This is why legal clarity must be part of your financial planning—not an afterthought.

Strategic Loan Planning: What Smart Buyers Do Differently

Experienced buyers structure loans, they don’t just take them.

They:

- Get pre-approved before finalizing property

- Maintain EMI within safe limits

- Keep liquidity buffer for 6–12 months

- Choose lenders based on flexibility, not just rates

- Plan prepayments early to reduce interest burden

A well-structured loan reduces stress and improves long-term wealth creation.

Final Perspective

In Gurgaon’s real estate market, most financial stress does not come from property prices—it comes from poorly structured loans.

A home loan is not just a financing tool. It is a long-term financial commitment that requires the same level of evaluation as the property itself.

If you want to align your purchase with long-term wealth creation, explore best investment strategy in Gurgaon real estate.

Because in Gurgaon:

Buying property is a decision.

Financing it correctly is a strategy.

Frequently Asked Questions (Home Loan in Gurgaon – 2026)

What salary is required to get a ₹1 crore home loan in Gurgaon?

Answer: To qualify for a ₹1 crore home loan in Gurgaon, most lenders expect a combined monthly household income of approximately ₹1.8 lakh to ₹2.2 lakh, depending on existing EMIs and credit profile.

Banks evaluate your debt-to-income ratio carefully, especially in high-ticket markets like Gurgaon. Ideally, total EMIs should not exceed 40–50% of your net monthly income. Applicants working with established corporate employers, IT firms, or reputed companies generally receive smoother approvals compared to unstable or irregular income profiles.

How much down payment is required for a ₹1.5 crore property in Gurgaon?

Answer: For a ₹1.5 crore property in Gurgaon, buyers typically need to arrange around ₹40–₹55 lakh upfront, including stamp duty and registration charges.

Banks usually finance 70–75% of the property value in this bracket. The remaining 25–30% must be arranged as margin money. Stamp duty, registration, and other transaction costs are paid separately and are not funded by the lender. Underestimating the total upfront cash requirement is one of the most common mistakes buyers make.

Is it risky to take a home loan for under-construction property in Gurgaon?

Answer: A home loan for an under-construction property in Gurgaon carries moderate risk, particularly if the project faces delays or liquidity issues.

Banks disburse funds in stages linked to construction progress. Buyers may pay pre-EMI during this period, which increases total interest outgo if possession is delayed. Choosing RERA-registered projects, reputed developers, and construction-linked payment plans reduces risk significantly.

Do banks finance builder floors easily in Gurgaon?

Answer: Banks do finance builder floors in Gurgaon, but approvals depend heavily on documentation quality and compliance.

Lenders verify land title clarity, approved building plans, completion certificates, and floor-wise registry structure. In certain independent floor projects, LTV may be lower compared to high-rise apartments from established developers. It is advisable to confirm lender approval status before committing to booking amounts.

Should I choose a bank or NBFC for a high-ticket home loan in Gurgaon?

Answer: Banks usually offer slightly lower interest rates, while NBFCs may provide faster approvals and greater flexibility for complex profiles.

For high-ticket home loans in Gurgaon, banks tend to apply stricter income assessment and conservative LTV policies. NBFCs may accommodate higher loan sizes or self-employed applicants more easily, though sometimes at a marginally higher interest rate. The right choice depends on borrower profile, urgency, and flexibility requirements rather than rate alone.

Join The Discussion