Gurgaon NCR has evolved into India’s most institutionally driven commercial real estate market. What began as a corporate spillover zone from Delhi is now the country’s most structured Grade A office and high-street commercial ecosystem.

As we move into 2026–2030, the future of commercial real estate in Gurgaon is no longer about speculative buying. It is about rental yield stability, micro-market intelligence, institutional-grade supply, and infrastructure-led capital appreciation.

For investors evaluating commercial property investment in Gurgaon in 2026, this period represents a selective — but potentially rewarding — cycle.

How Gurgaon Reached Structural Maturity

By 2025, Gurgaon had become NCR’s largest office absorption market. Strong demand from global occupiers, REIT-backed developments, and infrastructure expansion along NH-48 and Golf Course Road created a durable commercial backbone.

Unlike many Tier-1 cities, Gurgaon’s private-sector-led evolution enabled:

- Vertical expansion

- Mixed-use integration

- Early Grade A institutional development

- Flexible commercial zoning

Between 2023–2025, Gurgaon’s annual gross office absorption averaged approximately 8–10 million sq. ft., with vacancy levels gradually compressing in prime corridors such as Cyber City and Golf Course Road.

Looking ahead to 2026–2028, new Grade A supply is expected to remain measured relative to demand in core zones, while emerging corridors may witness staggered completions aligned with infrastructure execution.

The next phase is not expansion — it is optimization.

Gurgaon Commercial Real Estate Cycle Position (2026)

Understanding cycle stage is critical for capital allocation.

2010–2015: Expansion Phase

Rapid supply creation along NH-48 and Cyber City. Corporate entry accelerated leasing activity.

2016–2020: Oversupply & Correction

Vacancy expanded in select micro-markets. Rental growth moderated. Capital appreciation slowed in non-core assets.

2021–2024: Recovery & Institutional Consolidation

REIT participation increased. Lease tenures strengthened. Institutional-grade inventory began outperforming secondary supply.

2026–2030: Yield Discipline & Quality Filtering

Investor focus shifts toward income-producing commercial assets, tenant quality, ESG compliance, and infrastructure-backed corridors.

This is no longer a speculative growth market. It is a filtering market.

Office Space Demand (2026–2030): Flight to Grade A Quality

The office market is transitioning from quantity to quality.

Demand between 2026 and 2030 is expected to concentrate in:

- Grade A commercial inventory

- ESG-compliant office buildings

- Managed office space formats

- Transit-linked business districts

Hybrid work has not reduced structural demand. Instead, it has triggered consolidation into better buildings — strengthening high-quality institutional assets.

Micro-Market Outlook (With Risk Lens)

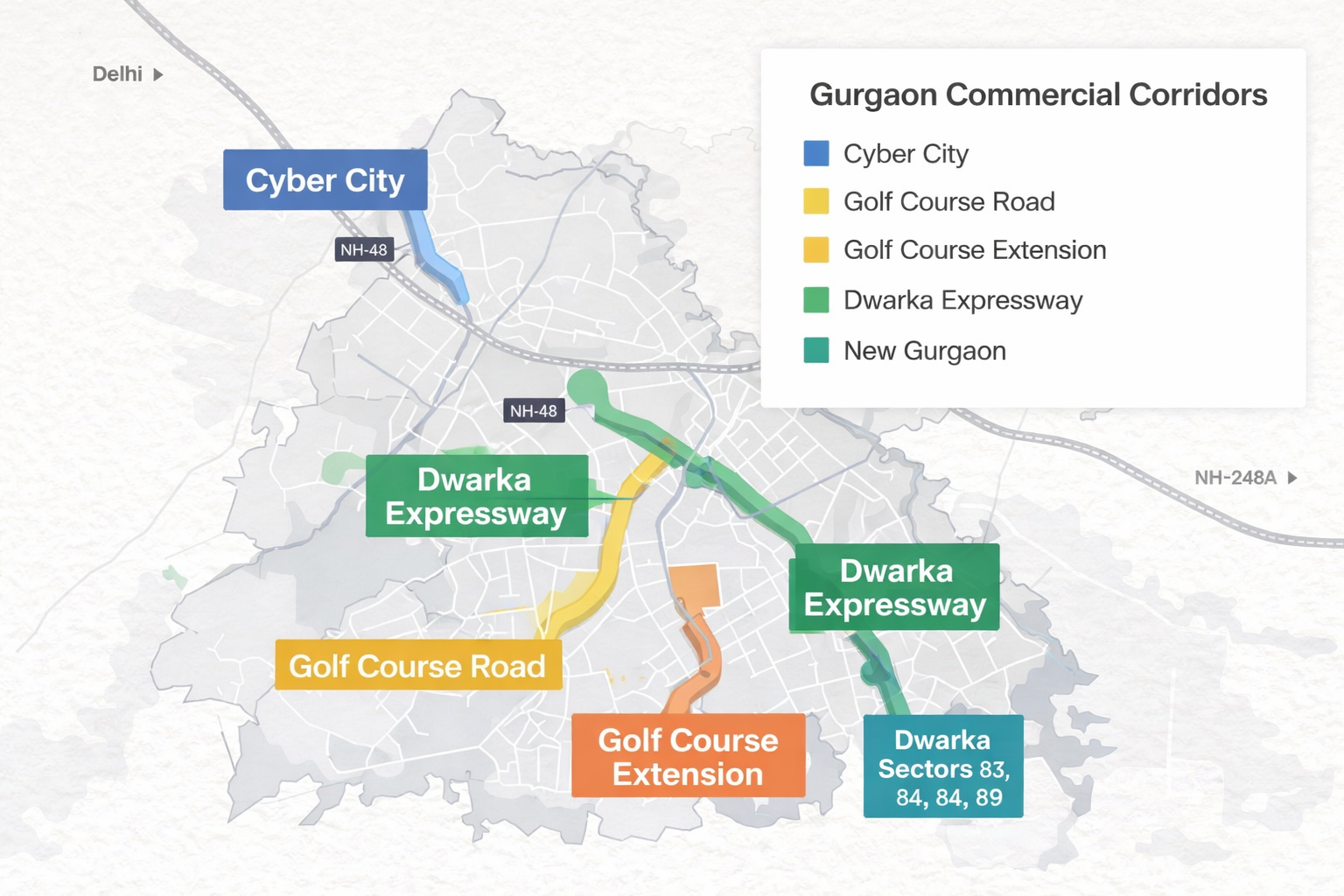

Cyber City & Golf Course Road

Remain core income-producing corridors. Rental growth may average 5–7% annually, with yields stabilizing in the 6–6.5% band. However, yield compression upside is limited due to already premium pricing.

Golf Course Extension Road

Golf Course Extension Road Emerging institutional corridor with improving absorption. Attractive for mid-ticket strata office investments, though lease stabilization timelines vary by asset quality.

Dwarka Expressway Commercial Property (2026 Cycle)

Early-stage capital appreciation potential remains strong. However, performance is infrastructure-execution dependent.

New Gurgaon Commercial Sectors (83–89)

New Gurgaon Retail-led commercial formats are gaining traction. Rental velocity remains sensitive to residential density maturation timelines.

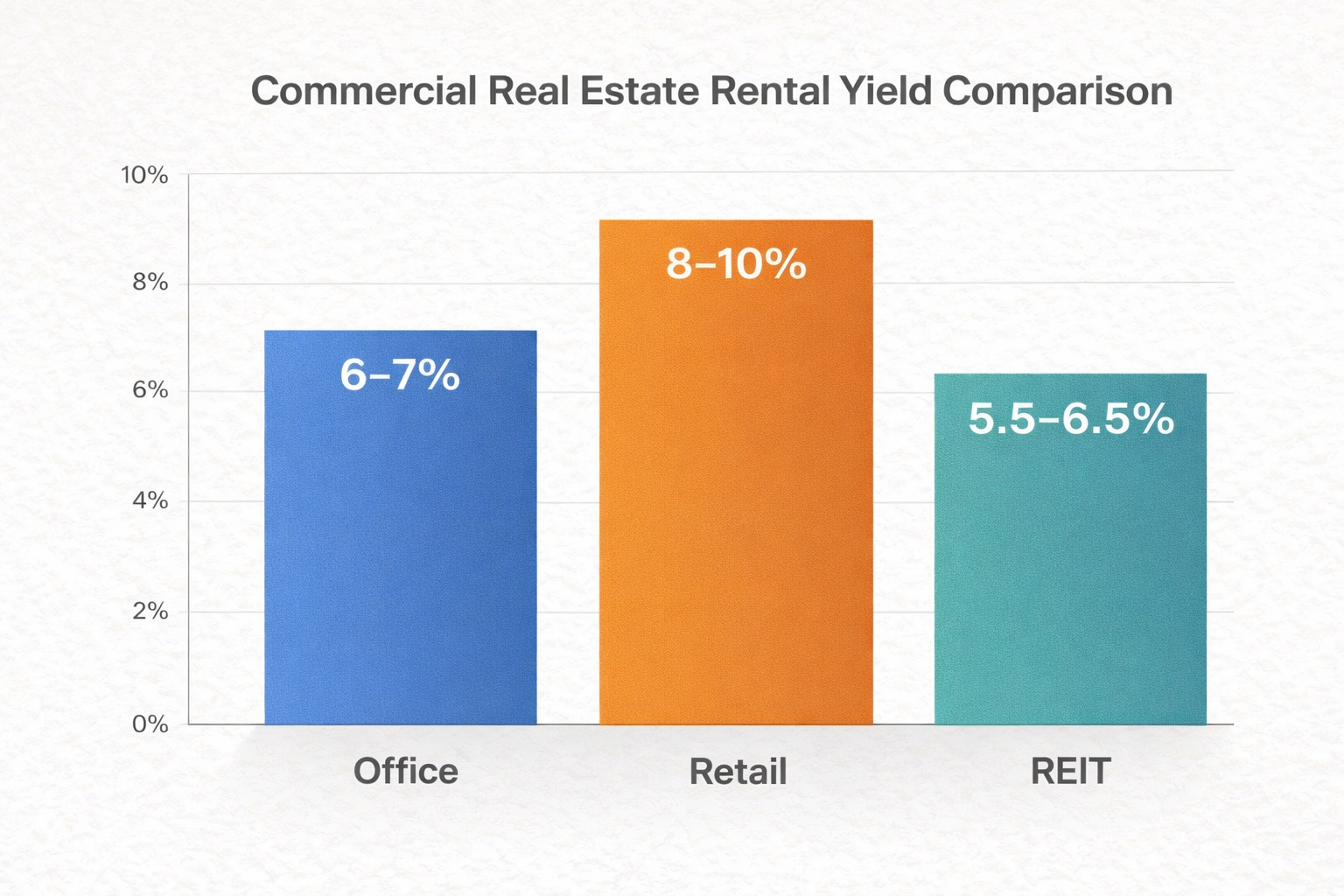

Rental Yield Outlook (2026–2030)

One of the fastest-growing investor queries remains:

“Commercial rental yield in Gurgaon 2026”

Expected Yield Bands

Core Grade A Office → 6–7%

Emerging Office Corridors → 7–8%

High-Street Retail → 8–10% (risk-adjusted)

REIT Exposure → 5.5–6.5%

Rental growth in prime zones may outpace capital appreciation.

In emerging corridors, capital values may rise faster initially before yield stabilization.

Retail Commercial Property: Density-Driven Growth

Retail-led commercial formats are entering a structural revival phase.

Demand is increasingly linked to:

- Residential catchment density

- Daily-need ecosystem integration

- F&B clustering

- Healthcare and education traffic drivers

Large-format malls remain relevant, but high-visibility, main-road-facing high-street formats are outperforming in yield terms.

For investors in the ₹1–3 Cr band, retail-led commercial assets offer relatively higher yield potential with moderate risk — provided location fundamentals are strong.

Institutional Capital & REIT Influence

Institutional participation is reshaping Gurgaon’s commercial landscape.

Increased REIT-backed ownership has:

- Reduced speculative supply

- Improved lease structures

- Increased governance transparency

- Stabilized cap rate expectations

Institutionalization reduces volatility and improves exit liquidity.

For HNI and NRI investors, alignment with institutionally preferred assets reduces downside risk.

Supply Pipeline & Risk Factors (2026–2030)

Despite strong fundamentals, risks remain.

Key considerations:

- Oversupply in micro-markets without absorption depth

- Delays in infrastructure execution

- Construction cost escalation

- Substandard Grade B inventory

Not all commercial assets will appreciate equally.

Quality filtering will intensify.

Who Should Avoid Commercial Investment in Gurgaon (2026–2030)

This cycle does not favor:

- Short-term flippers expecting rapid exits

- Over-leveraged investors dependent on aggressive financing

- Buyers chasing unrealistic 12–14% guaranteed yields

- Investors ignoring lease tenure, lock-in period, and tenant profile

Mature markets reward informed capital — not impulsive entry.

Investor Strategy Framework

₹50L–1Cr Ticket

Emerging retail formats

Early-stage commercial pockets

₹1–3Cr Ticket

Pre-leased institutional-grade units

Mid-sized high-street formats

₹3Cr+ Ticket

Large-format office floors

Core rental income assets

Diversification across corridors reduces exposure to single-market cycles.

Final Outlook: Strong but Selective Growth

The future of commercial real estate in Gurgaon (2026–2030) remains structurally positive — but increasingly selective.

Demand drivers remain intact:

- Corporate expansion

- Startup ecosystem growth

- Retail consumption

- Infrastructure execution

- Institutional capital inflow

However, the era of indiscriminate buying is over.

The next phase belongs to:

- Micro-market intelligence

- Rental yield discipline

- Infrastructure tracking

- Asset quality evaluation

Gurgaon is not peaking.

It is maturing.

Frequently Asked Questions (FAQs) – Commercial Real Estate in Gurgaon (2026–2030 Outlook)

Is commercial real estate in Gurgaon still a good investment in 2026?

Yes — but the nature of opportunity has changed. Gurgaon is now in a maturity phase, not a speculative boom phase. Investors focusing on institutional-grade assets, strong lease structures, and infrastructure-backed corridors can still achieve stable rental income and moderate capital appreciation between 2026–2030. The cycle now rewards discipline over aggressive speculation.

What rental yield can I realistically expect from commercial property in Gurgaon?

In the current cycle, realistic yield bands are:

Core Grade A office: ~6–7%

Emerging office corridors: ~7–8%

High-street retail (risk-adjusted): ~8–10%

REIT exposure: ~5.5–6.5%

Yield sustainability depends more on tenant quality, lease lock-in period, and entry pricing than headline percentages.

Which areas in Gurgaon are considered safer for long-term commercial investment?

Stability-oriented investors typically prefer established corridors like Cyber City and Golf Course Road due to strong institutional demand. Emerging corridors such as Golf Course Extension Road and Dwarka Expressway may offer higher growth potential, but returns are more sensitive to infrastructure execution and absorption timelines. Diversification across micro-markets reduces overall risk.

Is hybrid work reducing office demand in Gurgaon?

Hybrid work has changed office usage patterns but has not structurally reduced demand in prime locations. Instead, it has increased demand for better-quality buildings — ESG-compliant offices, transit-linked locations, and collaborative layouts. Institutional-grade commercial inventory is benefiting, while outdated Grade B supply faces pressure.

Who should avoid investing in Gurgaon commercial real estate in 2026–2030?

This cycle may not suit:

Short-term flippers expecting quick capital gains

Highly leveraged investors dependent on aggressive financing

Buyers chasing unrealistic 12–14% guaranteed returns

Investors ignoring lease tenure and tenant strength

The 2026–2030 phase rewards patient, research-driven capital allocation rather than speculative entry.

Join The Discussion