A data-backed, scenario-modeled outlook for serious buyers and capital allocators.

Between 2026 and 2031, price movement across Gurgaon, Sohna, and Manesar will not be uniform. The cycle is shifting from broad-based appreciation to micro-market precision — where sector-level absorption, rental resilience, and infrastructure maturity determine performance.

This report integrates historical trend anchors, forward-looking CAGR modeling, and risk scenarios to help investors make allocation decisions — not assumptions.

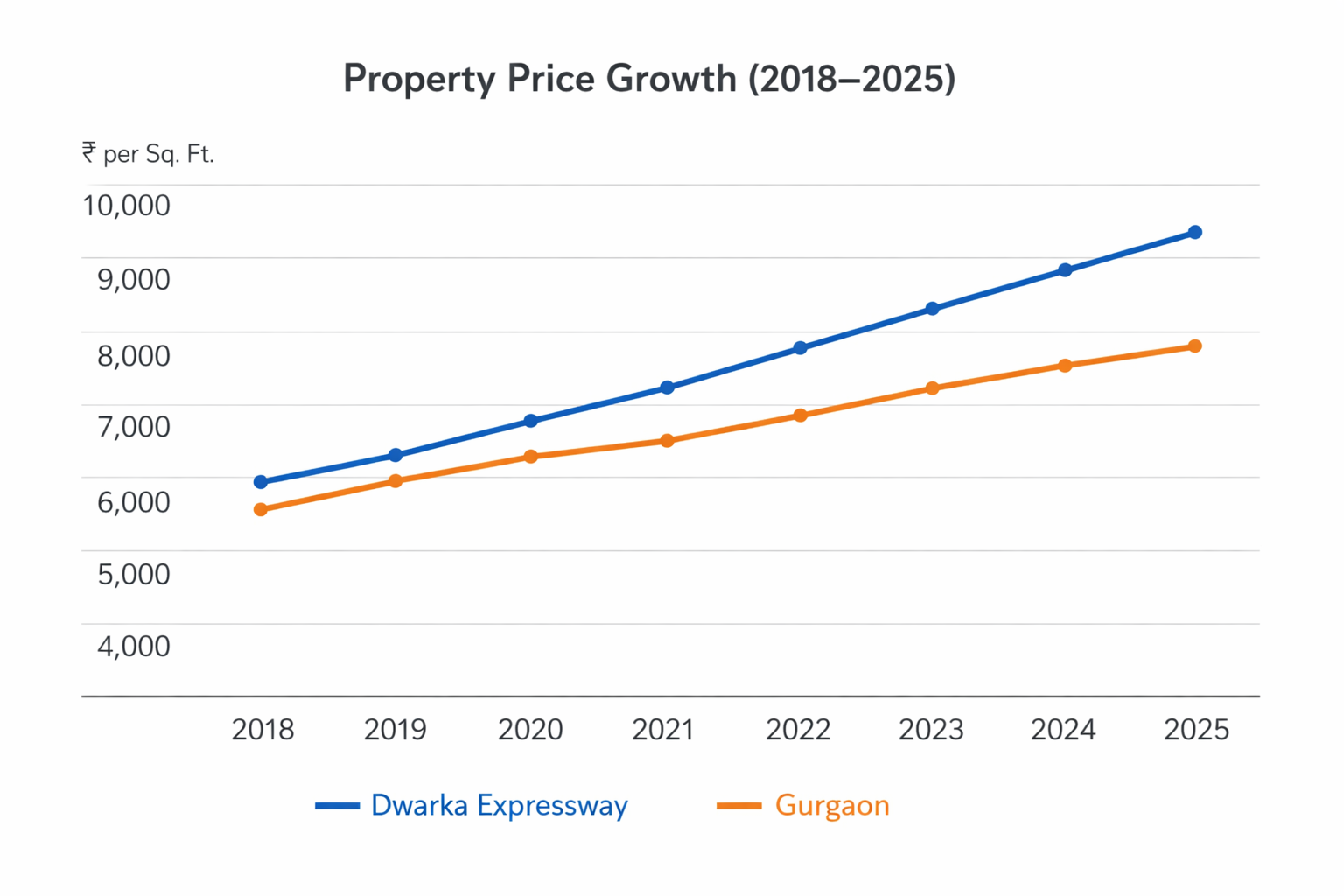

1. Historical Performance Snapshot (2018–2025)

Before forecasting forward, context matters.

Dwarka Expressway (2020–2025)

Select sectors along the corridor have seen cumulative price increases exceeding 60–90% as connectivity milestones materialized and speculative inventory transitioned toward end-user absorption.

Sohna (Pre-2020 vs 2025)

Once considered fringe, Sohna moved from entry-level pricing bands to structured mid-segment positioning, supported by improved road connectivity and growing residential supply.

New Gurgaon (2018 Overhang Phase → 2025 Stabilization)

Inventory overhang that once defined sectors 82–95 has gradually normalized, with rental occupancy improving and resale velocity strengthening.

This historical compression phase sets the base for the 2026–2031 outlook.

2. Gurgaon Outlook (2026–2031): From Core Stability to Corridor Acceleration

Prime clusters like Golf Course Road and established DLF zones are entering maturity. Annual appreciation in these ultra-prime markets may stabilize within the 8–12% range, reflecting pricing depth and reduced speculative elasticity.

The next wave lies in infrastructure-backed corridors.

Sector-Level Micro-Market Forecast

Investors tracking the Sector 67 Gurgaon price forecast for 2026–2031 are primarily evaluating mid-segment liquidity and resale turnover rather than launch momentum. Given strengthening absorption, a realistic CAGR expectation falls in the 10–13% range, assuming balanced supply.

In Sector 62, connectivity to Golf Course Extension Road provides structural demand stability, positioning it as a lower-volatility allocation within Gurgaon’s mid-premium bracket.

Along Dwarka Expressway, the Sector 102 price trajectory reflects improving end-user traction post-connectivity activation. Appreciation may realistically sustain 12–15%, contingent on commercial node activation.

Meanwhile, Sector 37D’s spillover potential depends on inventory tightening in more central expressway pockets. Price growth here could accelerate if absorption remains ahead of new launches.

Micro-market precision now outweighs “Gurgaon average” narratives.

Dwarka Expressway Price Forecast (2026–2031)

This corridor remains one of NCR’s most capital-sensitive investment belts.

Stabilization Phase (2026–2027)

Price normalization within the 10–12% annual band as speculative spikes settle.

Acceleration Phase (2028–2030)

Commercial activation + residential occupancy could lift appreciation toward the upper band of 12–16%, with upside scenarios approaching 18% only under strong infrastructure acceleration and rate easing.

Sector 102 vs Sector 113 Insight

- Sector 102: Balanced mid-premium demand, stronger rental depth.

- Sector 113: Higher-ticket positioning, potentially greater upside — but also higher volatility.

Investors projecting Dwarka Expressway price forecasts toward 2030 should evaluate liquidity and resale elasticity, not just launch pricing.

3. New Gurgaon (Sectors 82–95) Growth Trajectory

Sectors 82, 83, 90 and 95 are transitioning from early supply-driven narratives to occupancy-driven fundamentals.

Those evaluating future growth in Sector 82 Gurgaon or studying Sector 90 price potential toward 2027 are typically benchmarking:

- Rental compression trends

- Infrastructure maturity

- Developer balance sheet strength

Expected CAGR: 11–16%, with moderate risk tied to launch velocity.

4. Sohna: High-Growth but Higher Beta

Sohna’s transformation is no longer theoretical — it is structural.

Recent cycles delivered ~13% YoY growth. The next phase depends on execution timelines.

Deen Dayal Jan Awas Yojna (DDJAY) Outlook in Sohna

Low-rise DDJAY developments are attracting investors seeking plotted-style living with regulatory clarity.

Search behavior around DDJAY Sohna appreciation potential reflects rising confidence in low-density formats versus saturated high-rise inventory in central Gurgaon.

Projected CAGR: 12–16% base case, with upside toward 18% only under accelerated infrastructure and strong end-user migration.

Risk variable: Infrastructure slippage compressing absorption velocity.

5. Manesar: Industrial-Linked Residential Expansion

Manesar operates differently from Gurgaon’s luxury cycle.

Growth is employment-driven.

Residential clusters near IMT Manesar are witnessing steady absorption among industrial professionals. Investors analyzing IMT Manesar housing demand trends for 2026 are primarily assessing job hub stability.

Projected CAGR: 8–12%, with upside linked directly to industrial belt expansion and logistics ecosystem scaling.

6. Scenario Modeling (2026–2031)

Base Case (Most Likely)

- Gurgaon: 9–13% CAGR

- Sohna: 12–16% CAGR

- Manesar: 8–12% CAGR

Stable rates, steady job growth, moderate supply.

Bull Case

- Corporate expansion accelerates

- Rate cuts increase affordability

- NRI inflows strengthen

Outperforming sectors may approach 16–18%.

Risk Case

- Oversupply in mid-segment

- Liquidity tightening

- Slower income growth

CAGR compresses by 2–4 percentage points across markets.

This scenario framing improves forecast realism and credibility.

7. Micro-Market CAGR Snapshot (2026–2031)

| Micro Market | Est. CAGR | Demand Driver | Risk Factor | Liquidity Profile |

|---|---|---|---|---|

| Sector 67 Gurgaon | 10–13% | Mid-Segment Premium | Supply Elasticity | High |

| Sector 102 (Dwarka Expressway) | 12–15% | Infrastructure Maturity | Execution Risk | Moderate–High |

| Sohna DDJAY | 12–16% | Low-Rise + Affordability | Infra Timeline Risk | Moderate |

| IMT Manesar Belt | 8–12% | Industrial Workforce | Commercial Dependency | Moderate |

8. Capital Appreciation vs Rental Yield Reality (2026 Context)

While appreciation dominates investor narratives, rental yields in Gurgaon and Sohna generally remain between 2.5–4%.

This creates a familiar debate: capital appreciation vs rental yield optimization.

Investors allocating ₹1–3 Cr in 2026 should evaluate:

- Rental compression potential

- Vacancy resilience

- Resale liquidity depth

- Entry price sensitivity

Sector-level selection now matters more than city-level timing.

9. Strategic Allocation Insights

For end-users:

Emerging corridors like SPR and stabilized New Gurgaon sectors offer balance between pricing and infrastructure maturity.

For investors:

Mid-segment inventory with proven absorption history typically provides better exit liquidity than ultra-luxury positioning.

For long-term holders:

Connectivity nodes (metro stations, expressway junctions, commercial hubs) remain structurally advantaged.

Final Outlook

Between 2026 and 2031:

- Prime Gurgaon stabilizes.

- Expressway corridors differentiate.

- Sohna offers high-growth but higher volatility.

- Manesar delivers industrial-linked steady appreciation.

This cycle will reward micro-market intelligence over headline optimism.

Frequently Asked Questions (FAQs)

Will Gurgaon property prices really keep rising till 2031 or is the current growth cycle near its peak?

Gurgaon is unlikely to witness uniform, explosive growth across all sectors, but sector-level appreciation remains structurally supported by infrastructure maturity, employment expansion, and sustained premium housing demand. Prime central locations may stabilize into moderate growth bands, while emerging corridors such as Dwarka Expressway and New Gurgaon could continue delivering stronger appreciation under stable macroeconomic conditions. The market is shifting from speculative spikes to absorption-led price movement rather than nearing an abrupt peak.

Which micro-markets in Gurgaon have the highest 5-year appreciation potential?

Investors are increasingly focusing on sector-level fundamentals rather than city-wide averages. Corridors along Dwarka Expressway with improving occupancy and commercial activation show strong forward potential. Select sectors in New Gurgaon (82–95) are also benefiting from rental stabilization and infrastructure completion. Over the next five years, appreciation will depend more on inventory absorption and connectivity strength than on new launch momentum.

Is Sohna still a high-growth investment opportunity or has most of the upside already played out?

Sohna remains a higher-growth corridor compared to mature Gurgaon locations, but it also carries slightly higher volatility. While recent cycles delivered strong gains, the next phase depends on infrastructure delivery and sustained end-user migration. Low-rise developments under the Deen Dayal Jan Awas Yojna format continue to attract investors seeking lower entry bands and plotted-style living, keeping long-term appreciation potential intact.

How does Manesar compare to Gurgaon for long-term property investment?

Manesar follows an industrial-driven growth model rather than a luxury residential cycle. Its price trajectory is closely tied to employment expansion, logistics activity, and industrial occupancy. While appreciation may be more moderate compared to premium Gurgaon sectors, it offers steady growth potential supported by workforce demand and ecosystem development.

Should investors prioritize capital appreciation or rental yield in Gurgaon between 2026 and 2031?

Rental yields in Gurgaon and Sohna generally range between 2.5–4%, meaning capital appreciation remains the primary return driver. However, liquidity depth and rental resilience are becoming increasingly important as prices rise. Investors should evaluate sector-level absorption trends, resale potential, and entry pricing rather than focusing solely on headline CAGR projections.

Join The Discussion