Dwarka Expressway in Gurgaon has entered a fundamentally different phase in 2026. What was once a speculative growth corridor has now become an active capital allocation zone, and that shift is visible not just in infrastructure, but in how serious buyers are behaving.

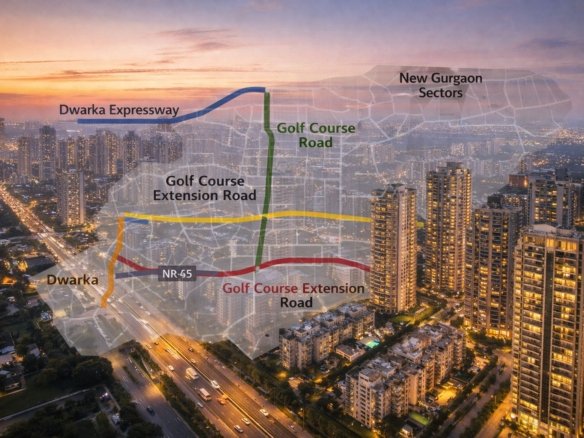

The 29-kilometre stretch connecting Mahipalpur in Delhi to Kherki Daula is now largely operational, which means investors are no longer betting on future connectivity. They are underwriting real, usable access to Delhi and the airport. If you place this corridor within the broader context of the Gurgaon investment location guide , its role has clearly evolved from peripheral to central.

This transition has also changed how it compares with the best sectors in Gurgaon. Earlier, it was seen as an emerging alternative. Today, in certain pockets, it is competing directly on pricing narratives and demand quality.

Why 2026 Feels Different

The biggest change is not just infrastructure completion. It is the shift in buyer psychology.

In 2025 and early 2026, several luxury launches in Sectors 113 and 114 saw strong absorption within initial phases. This is not typical for Gurgaon unless the underlying demand is both confident and capital-backed. The demand is being driven by a mix of West Delhi buyers upgrading into larger formats, NRIs preferring proximity to the airport, and investors positioning for long-term appreciation.

This aligns closely with what broader data suggests about the right time to buy property in Gurgaon. Once infrastructure becomes operational rather than speculative, pricing behaviour tends to stabilise at higher levels instead of fluctuating.

The Real Investment Story: Price Gap and Spread Compression

At the core of Dwarka Expressway’s investment thesis is a very simple idea — price gap.

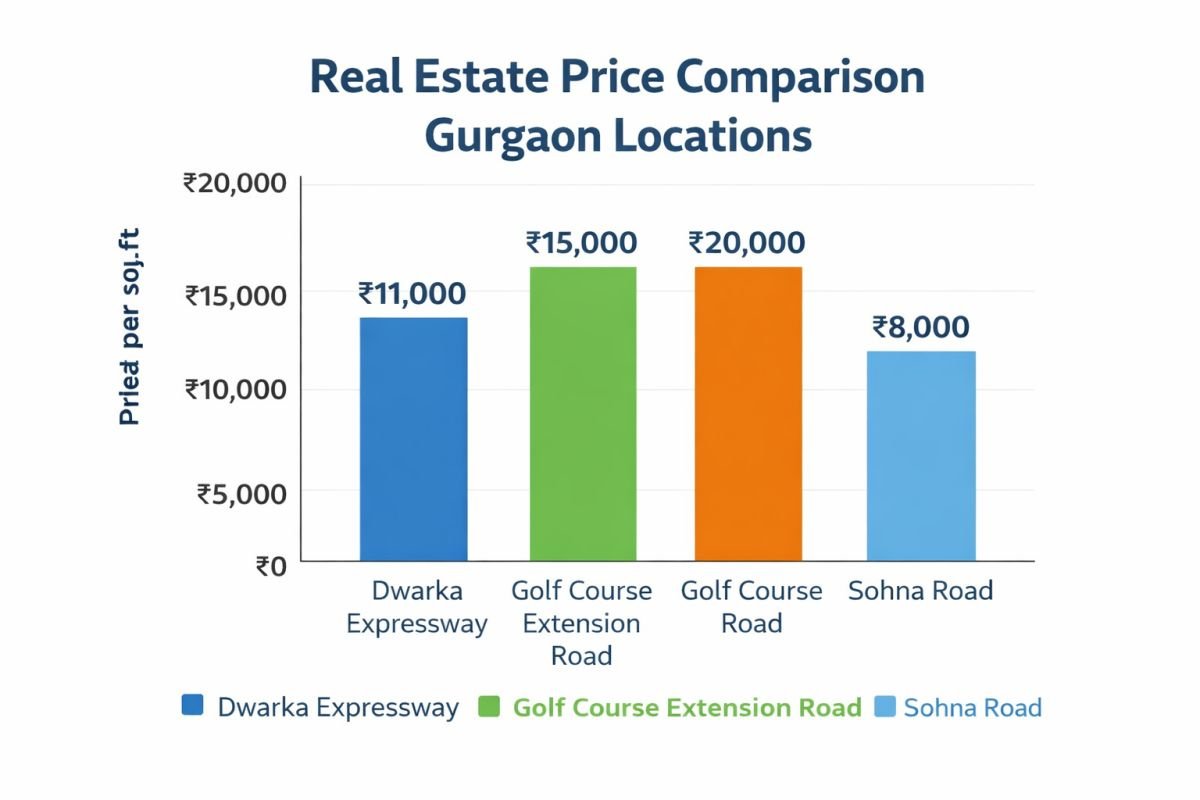

Prime Golf Course Road continues to trade between ₹22,000 and ₹25,000 per square foot, while premium projects in Sector 113 are currently priced between ₹16,000 and ₹18,000. Mid-segment sectors such as 102 to 109 are still available in the ₹13,000 to ₹15,000 range.

This ₹5,000 to ₹8,000 gap is what investors are focusing on. The assumption is not that Dwarka Expressway will match Golf Course Road immediately, but that even partial compression of this spread over the next few years can generate meaningful capital appreciation.

Price Movement: What the Data Actually Shows

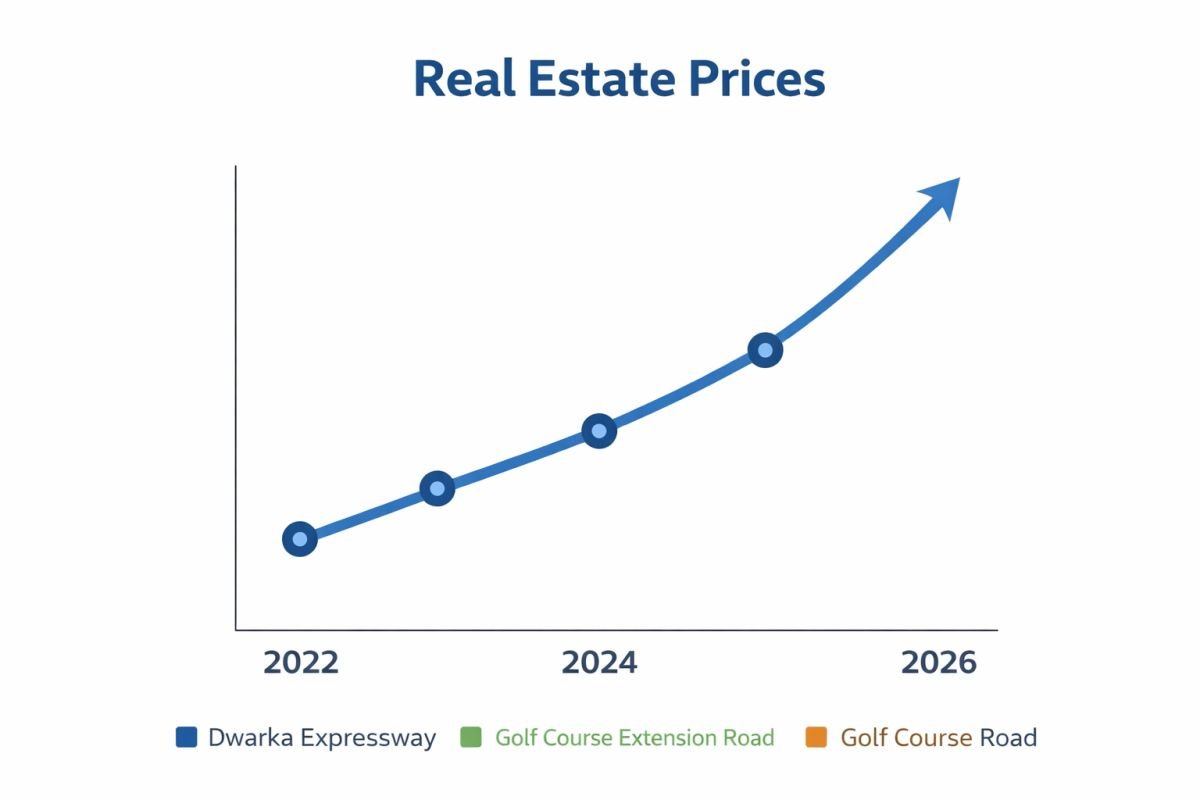

The price trajectory of this corridor tells a clear story of infrastructure-led re-rating.

In 2022, prices were largely in the ₹7,500 to ₹9,000 range. By 2024, they had moved to ₹10,000–₹13,000. In 2026, premium sectors are comfortably operating between ₹14,000 and ₹18,000 or higher.

What is more important than the price increase is the behaviour behind it. Despite rising ticket sizes, absorption has remained stable in selective launches. This indicates pricing strength rather than speculative overheating.

Price vs ROI Snapshot (2026)

| Micro-Market | Avg Price (₹/sq ft) | Appreciation Potential | Rental Yield | Risk Level |

|---|---|---|---|---|

| Sector 113 | 16,000 – 18,000+ | High (Spread Compression) | 2.8% – 3.2% | Moderate |

| Sector 114 | 15,000 – 17,000 | Strong | 2.7% – 3.0% | Moderate |

| Sector 111 | 15,000 – 17,500 | Stable–Strong | 2.6% – 3.0% | Balanced |

| Sectors 102–109 | 13,000 – 15,000 | Selective | 2.5% – 2.8% | High (Oversupply) |

The Truth About Micro-Markets (Where Most Investors Go Wrong)

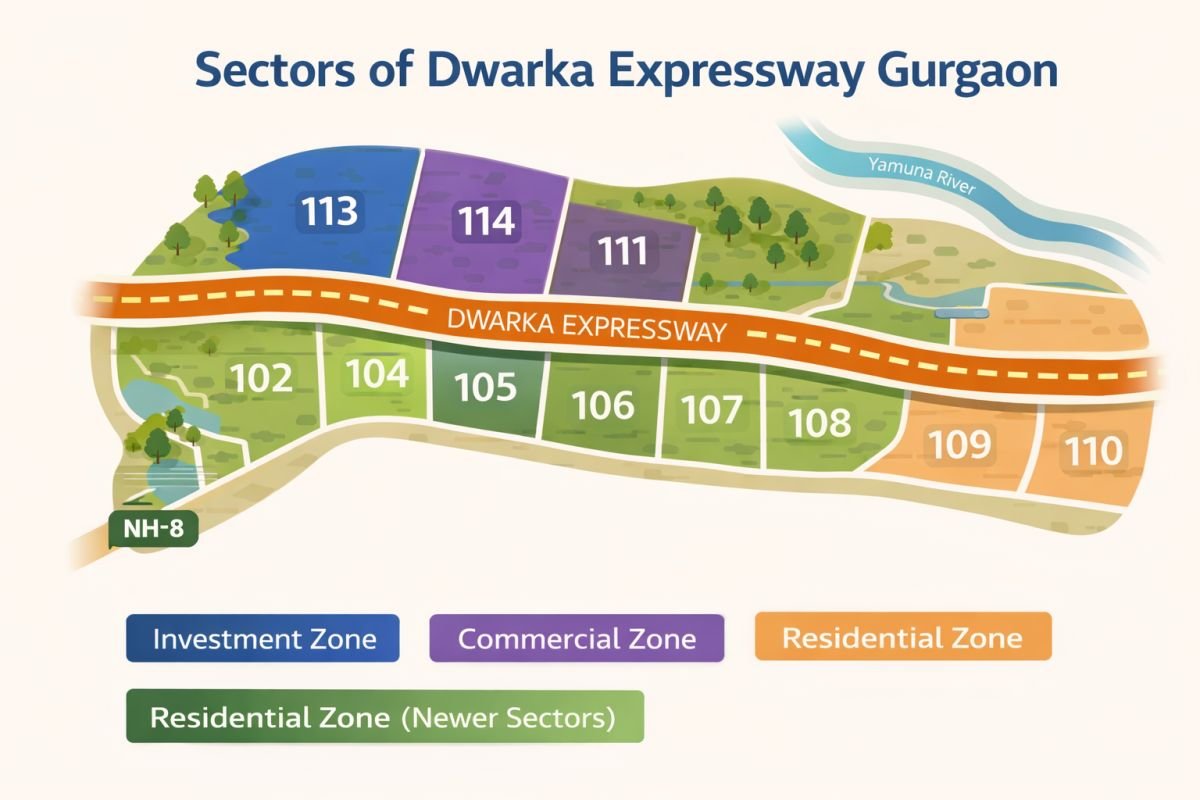

One of the biggest mistakes people still make is treating Dwarka Expressway as a single market. It isn’t. In reality, it behaves like three completely different ecosystems, each driven by its own demand and supply dynamics.

The Delhi-border belt covering Sectors 113 and 114 is driven by scarcity, proximity to Delhi, and premium positioning. Sector 111 acts as a transitional zone where buyers who are priced out of the top-end clusters still want access to similar infrastructure and lifestyle benefits. Meanwhile, the 102–109 stretch is a supply-heavy belt where pricing is influenced more by inventory levels than by positioning.

This kind of segmentation reflects the broader Gurgaon residential demand supply dynamics, where different micro-markets behave independently rather than moving in sync.

Sector-Level Analysis

Sector 113: The Core Luxury Cluster

Sector 113 is currently the most capital-intensive micro-market on Dwarka Expressway. Its biggest advantage is simple — it is the first major residential cluster when entering Gurgaon from Delhi.

Projects such as Smartworld One DXP and M3M Capital have positioned themselves as premium offerings, with prices ranging from ₹16,000 to ₹18,000 per square foot and 3BHK entry points starting around ₹3.5 crore.

The demand profile here is dominated by high-net-worth buyers from West Delhi, NRIs, and investors betting on long-term appreciation through spread compression. For buyers looking to explore actual inventory in this segment, Flats on Dwarka Expressway provide a direct view of available options.

From a capital perspective, this remains the strongest appreciation story in the corridor, although entry timing becomes important as more luxury launches enter the market.

Sector 114: Slightly Better Entry, Similar Story

Sector 114 shares many of the advantages of Sector 113 but offers slightly softer entry pricing. Current rates range between ₹15,000 and ₹17,000 per square foot, with 3BHK configurations starting around ₹3 crore.

This makes it attractive for buyers who want access to the same Delhi-border advantage without paying peak pricing. Investors exploring early-phase opportunities can look at New Residential Projects on Dwarka Expressway to identify projects still in favourable entry stages.

In terms of long-term positioning, Sector 114 is closely tied to the performance of Sector 113, which gives it a strong appreciation alignment.

Sector 111: The Transitional Zone

Sector 111 operates as a bridge between premium border sectors and the more supply-heavy interior clusters. Projects like M3M Crown reflect this positioning, offering premium amenities at slightly lower price points compared to the top-end segments.

Prices here generally fall between ₹15,000 and ₹17,500 per square foot. This makes it suitable for buyers who want a balance between lifestyle and entry cost. However, its performance is somewhat dependent on how strongly the border sectors continue to absorb supply.

Sectors 102–109: Opportunity With Conditions

The 102–109 belt is where the narrative becomes more complex. This region has the highest cumulative supply on Dwarka Expressway, including both new launches and legacy inventory.

Prices are comparatively lower, typically between ₹13,000 and ₹15,000 per square foot, and entry tickets are more accessible. However, this affordability comes with a trade-off — higher supply risk and less predictable appreciation.

Some projects launched in earlier cycles here are still catching up to the price growth seen in the border sectors. Buyers considering this segment should compare options across New Projects in Gurgaon to avoid being locked into underperforming inventory.

This is not a bad market, but it is a selective one. Stock picking matters more than location branding.

Entry Strategy: Timing Still Matters

Even in a matured corridor, entry timing plays a critical role. Pre-launch projects offer lower entry prices but come with execution risk. Under-construction projects provide a more balanced risk-reward equation, while ready-to-move inventory offers safety but limited upside.

Investors should not rely purely on pricing discounts. Entry decisions need to align with broader timing insights such as those discussed in the right time to buy property in Gurgaon, where cycle positioning plays a major role in outcomes.

What Happens Next: 2027–2030 Outlook

Looking ahead, Dwarka Expressway is likely to evolve into a more structured and differentiated market. Border sectors may develop into a high-end residential cluster with strong identity, while transitional zones like Sector 111 continue to offer balanced growth. The 102–109 belt will likely see selective appreciation depending on how supply gets absorbed.

The era of uniform growth across the corridor is over. Future returns will depend on micro-market selection, project quality, and entry timing.

Where Should You Look Next?

For someone seriously evaluating Dwarka Expressway, the next step is not just understanding the corridor but narrowing down the right segment.

Buyers focused on premium positioning should explore border sectors such as 113 and 114. Those looking for a balance between pricing and lifestyle can consider Sector 111, while value-driven investors need to carefully filter opportunities within the 102–109 belt.

To explore curated and verified options across segments, you can review Best Upcoming Projects in Gurgaon, which provides a broader comparison across micro-markets.

Final Takeaway

Dwarka Expressway is no longer about discovering opportunity. That phase is over.

What remains now is selection.

The corridor has matured, pricing has adjusted, and demand has stabilised. From here onward, outcomes will depend less on the corridor itself and more on where and how you enter it.

In 2026, this is no longer a speculative bet.

It is a strategic decision.

FAQs – Upcoming Projects on Dwarka Expressway 2026

Is Dwarka Expressway a good investment in 2026?

Dwarka Expressway in 2026 is considered a structurally stronger market compared to previous years because the connectivity is now operational rather than speculative. The corridor benefits from direct Delhi access and improved airport connectivity, which has shifted buyer confidence significantly. That said, investment quality depends on sector selection. Border sectors such as 113 and 114 show stronger long-term positioning, while mid-segment belts require more careful project-level evaluation. It is no longer about investing in the entire corridor — it is about choosing the right micro-market.

Which sector is best to invest in on Dwarka Expressway in 2026?

The answer depends on your objective. Sector 113 currently carries the strongest positioning due to its Delhi-entry advantage and luxury cluster development. Sector 114 offers similar connectivity benefits with slightly softer entry pricing. Sector 111 provides balanced exposure for buyers who want premium living without peak-border pricing. Sectors 102–109 may offer selective value, but supply density is higher and must be evaluated carefully. There is no single “best” sector — only the one that aligns with your capital strategy.

What are the current property rates on Dwarka Expressway in 2026?

Property rates on Dwarka Expressway in 2026 vary by micro-market. Premium border sectors such as 113 and 114 are generally ranging between ₹15,000 and ₹18,000 per sq ft, with some luxury configurations exceeding that. Sector 111 typically falls within ₹15,000 to ₹17,500 per sq ft depending on project positioning. The 102–109 belt remains comparatively more affordable, usually between ₹13,000 and ₹15,000 per sq ft, though pricing differs based on construction stage and developer profile.

What is the price of a 3BHK apartment on Dwarka Expressway in 2026?

In prime border sectors like 113 and 114, luxury 3BHK units typically begin around ₹3 crore and can extend beyond ₹4.5 crore depending on unit size and project density. In transitional or mid-segment sectors such as 102–109, 3BHK configurations may start closer to ₹2 crore to ₹3 crore. Buyers should assess not just base price, but also delivery timelines, amenities, and supply competition within that sector.

Are pre-launch projects on Dwarka Expressway safe for investment?

Pre-launch projects can offer lower entry pricing, but they require careful due diligence. Investors should verify RERA registration, land title status, phase approvals, and the developer’s delivery history before committing funds. Established developers with structured launch cycles generally carry lower risk compared to purely marketing-driven speculative offerings. Pre-launch entry works best when backed by execution clarity rather than only price advantage.

What rental yield can investors expect on Dwarka Expressway properties?

Rental yields in 2026 are moderate rather than aggressive. Premium border sectors typically offer estimated gross yields between 2.5 percent and 3.2 percent, depending on unit configuration and proximity to commercial hubs. The corridor is largely viewed as a capital appreciation market rather than a high-yield rental zone. Buyers focused primarily on rental income should factor in long-term leasing demand and supply levels within their chosen sector.

Will property prices on Dwarka Expressway continue to rise after 2026?

Future appreciation is expected to be sector-specific rather than uniform across the entire corridor. Border luxury clusters may continue benefiting from pricing spread compression compared to established premium corridors in Gurgaon, provided supply remains disciplined. However, areas with higher inventory concentration could experience slower price movement. Long-term growth will depend on infrastructure consolidation, commercial ecosystem development, and launch discipline over the next few years.

Join The Discussion